The faint glow of a smartphone screen illuminates a late-night purchase, a transaction that would have been unthinkable just a few years ago. This isn’t just about convenience anymore; it’s a fundamental platform shift, and AI is the engine driving it.

Look, we’ve all felt it, right? The internet economy has been churning, evolving at warp speed, and now businesses are being forced—or perhaps, inspired—to architect their checkout experiences with a level of personalization previously reserved for bespoke tailoring. Stripe’s data paints a vivid picture: a staggering 65% of transactions under fifty bucks now zip through on mobile. But here’s the kicker—shoppers aren’t just browsing or grabbing coffee money on their phones anymore; they’re staying put for heftier purchases, too. Digital wallets, those sleek conduits of digital commerce, are whittling down average mobile checkout times by a whopping half. Yet, this isn’t a one-size-fits-all utopia; wallet preferences splinter wildly across regions and generations, dictating the very shape and feel of the checkout flow.

And then there are local payment methods. They’re not just nice-to-haves anymore; they’re becoming titanic drivers of conversion. Offering the right local flavor—or, more likely, the right complex blend—can unlock a significant bump in performance. It’s like speaking the customer’s native tongue, not just in language, but in currency and custom.

But here’s where things get truly mind-bending: checkout is being fundamentally redesigned for an entirely new kind of buyer. Meet the agents. As consumers grow increasingly cozy with AI-assisted purchasing across a dizzying array of product categories, businesses are scrambling to re-architect their risk management frameworks and, more importantly, convert an ever more fragmented demand stream.

Mobile’s Mammoth March Upward

Mobile already rules the small-ticket kingdom, that much is clear. But the old playbook, the one where big-ticket purchases meant a reluctant shuffle to the desktop, is starting to gather dust. Stripe’s analytics reveal a dramatic trend: shoppers are increasingly comfortable clicking ‘buy’ on higher-value items—yes, even those tipping over the $500 mark—right from their mobile devices. This metamorphosis is particularly pronounced in the Asia-Pacific and EMEA regions, where mobile isn’t just a device; it’s the primary gateway to digital interaction. Even here in the US, mobile has steadily clawed back market share across every purchase bracket we’ve tracked over the past two years. Canada remains an interesting outlier, with shoppers there still showing a propensity to pivot to desktop when purchases hover between $100 and $249. It’s a fascinating peek into regional digital habits.

The Global Wallet Game: A Generational, Regional Riddle

Digital wallets have officially transcended niche status; they now command roughly 30% of the global point-of-sale volume. Our surveys echo this sentiment: a solid 61% of shoppers worldwide declared their willingness to embrace digital wallets. And in markets historically tethered to the trusty plastic card, like the US and Japan, these digital conduits are emerging as some of the most rapidly ascendant checkout methods. This is where the generational chasm becomes starkly apparent. Younger demographics, those digital natives we often talk about, are not just comfortable but eager to use wallets for everything. It’s not just about small indulgences either; the data suggests a significant portion of younger users are wielding wallets for purchases well into the hundreds of dollars.

The speed advantage is undeniable. Stripe’s data consistently shows that employing a digital wallet can slash mobile checkout times by a staggering 50%. However, while wallets are rapidly becoming the default layer of interaction in many markets, identifying the dominant player remains a regional guessing game. From MB WAY in Portugal to MobilePay in Denmark, and the ubiquitous Alipay in China, these localized champions dictate how businesses must architect their checkout flows. Simply supporting Apple Pay, Google Pay, and Link might suffice in some locales, but in others, a entirely different wallet constellation is required to truly capture consumer attention and drive conversion.

Localizing Trust in a Fragmented World

Global demand is fantastic, a clear indicator of market reach. But global demand doesn’t automatically translate into completed sales. Businesses now face the complex challenge of localizing checkout, and even that localization strategy is far from uniform. What a customer expects from their checkout experience can vary wildly from one nation to the next. In regions like Indonesia and Vietnam, payment preferences are a vibrant mosaic, spread across digital wallets, bank transfers, debit-linked apps, and a rich mix of other local methods. Here, true localization means an overhaul of the entire experience: the payment mix, the currency display, and how options are presented. It’s about building trust through familiarity.

Conversely, in other markets, preferences are far more consolidated. Success hinges on placing a single, dominant payment method front and center. Our experiments on the Stripe network are eye-opening: just presenting one payment method that’s out of step with the local preference can crater conversion rates by as much as 15%. The impact of nailing the local favorite is profound. Offering BLIK to Polish customers, for instance, has been shown to boost checkout conversion by an average of 46%. Similarly, Pix in Brazil has driven conversion increases of 31% on average. It’s a powerful demonstration that speaking the local payment language is non-negotiable.

The Dawn of Agent-Assisted Commerce

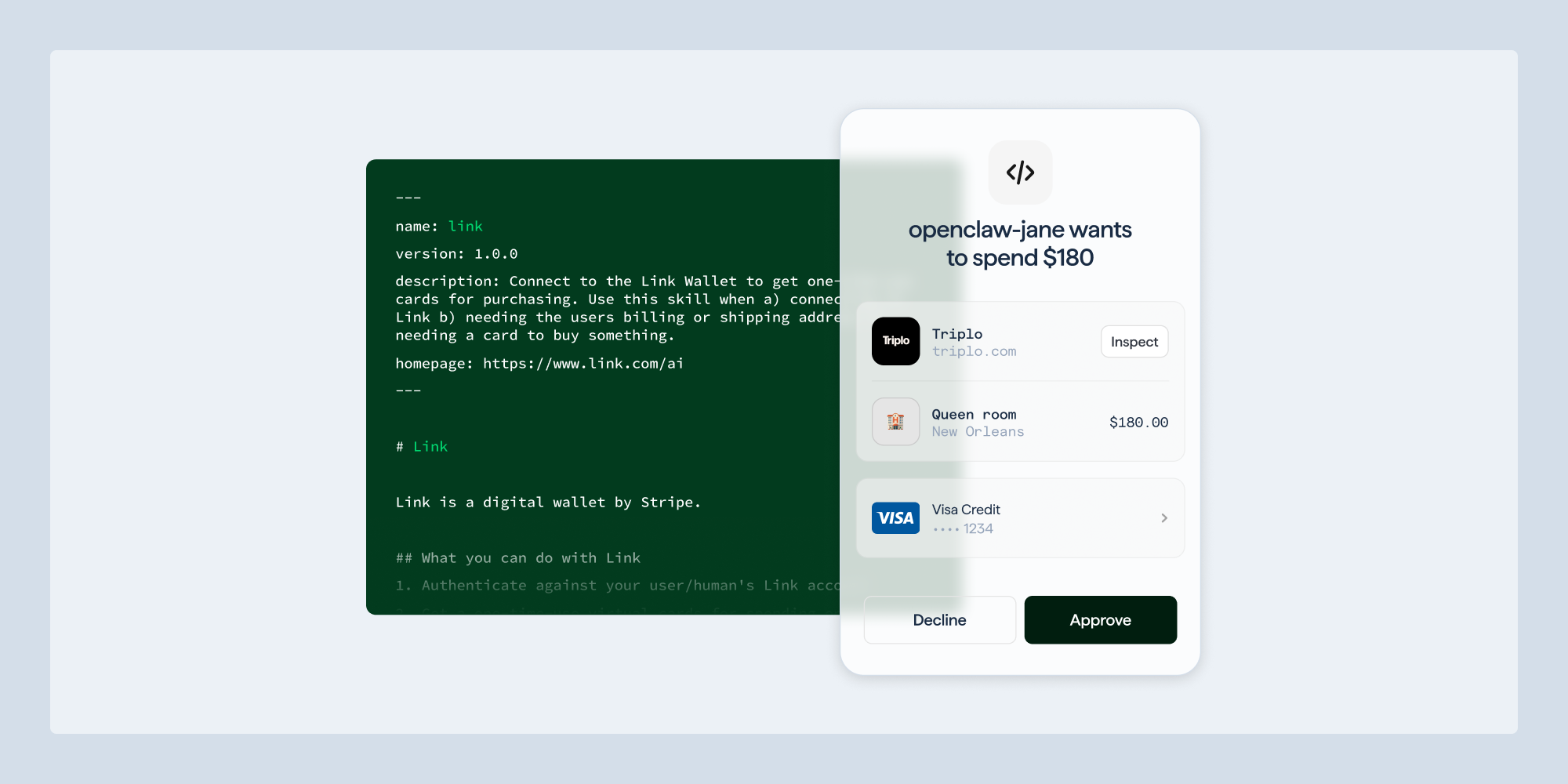

AI isn’t just a backend optimization tool anymore; it’s actively reshaping the entire journey to checkout. On the consumer-facing side, shoppers are growing increasingly receptive to the idea of an agent—an AI assistant—guiding them through their purchasing decisions. Surveys, like the one conducted by Stripe and Visa, reveal a majority of consumers across markets are open to this kind of AI-driven assistance. It’s a seismic shift from the days of solo browsing to a collaborative buying experience.

But the back-end story is equally compelling. As AI agents become more sophisticated, they’ll need dedicated checkout interfaces, ones that can handle complex, multi-step transactions, manage returns, and even negotiate pricing. This isn’t science fiction; it’s the next frontier of e-commerce, where the very definition of ‘customer’ is expanding to include intelligent entities.

My unique insight here? We’re witnessing the birth of what I call “Probabilistic Checkout.” It’s not just about offering the right payment method; it’s about offering the predicted payment method, the trusted agent, the expected next step, based on a sophisticated understanding of context—device, location, past behavior, and even the perceived intent of an AI agent. This isn’t merely an evolution; it’s a revolution in how value is exchanged online.

The core thesis emerging from Stripe’s analysis is that trust, in its most granular, localized, and intelligently presented form, is the ultimate currency of the modern checkout. Businesses that can master this nuanced approach will not just survive; they will thrive in this new, AI-powered landscape.

🧬 Related Insights

- Read more: SBI Holdings Eyes Bitbank: Japan Crypto Consolidation Heats Up

- Read more: HB Wealth Dumps Spreadsheets for Arch to Dominate Private Markets

Frequently Asked Questions

What are AI agents in shopping? AI agents are sophisticated programs designed to assist shoppers with tasks like product discovery, comparison, and even making purchases, acting as a digital shopping assistant.

Will AI agents replace human customer service? While AI agents can handle many routine queries and transactions, complex issues and nuanced customer interactions will likely still require human oversight and intervention.

How do digital wallets improve checkout speed? Digital wallets store payment and shipping information securely, allowing users to complete purchases with fewer clicks and less manual data entry, significantly reducing checkout time.