Forget AI for a minute. Let’s talk about numbers that actually make your eyes water: Some analysts are throwing around the figure of $10 trillion for the potential size of tokenized asset markets by 2030. Think about that. That’s not pocket change; that’s enough to make your hair stand on end. And the engine behind this theoretical gold rush? “Tokenized composability.” Sounds fancy, right? It’s basically the idea of taking digital tokens that represent real-world assets — stocks, bonds, real estate, whatever — and chaining them together, stacking them up like financial Lego bricks to create new, complex products. The pitch is that this will unlock unprecedented innovation, much like how combining maps, payments, and driver locations birthed Uber. Except, you know, with trillions of dollars.

And here’s the thing, after two decades watching this circus, that ‘magic’ ingredient often turns out to be… well, a very clever way for someone to make a lot of money off someone else’s risk. The people selling the dream rarely highlight the fallout when the structure inevitably wobbles.

This isn’t exactly a new song and dance. We saw it with securitization, the granddaddy of financial engineering that fueled the 2008 meltdown. Wrap up a bunch of mortgages, slice ‘em up, sell ‘em off, repeat. Sound familiar? Apparently, history doesn’t just rhyme; it occasionally does a full-on cover song with slightly different synth sounds.

Is This Just Old Wine in a Shiny New Token Bottle?

Tokenized composability, in theory, means taking a tokenized asset and dropping it into another tokenized product, which then becomes a component for yet another. Each piece is supposed to be understandable on its own. The real juice – and the real danger – is in how they’re all bolted together. The SEC is right to be cautious, dawdling its way through this. They’ve seen this movie before, and the ending wasn’t pretty.

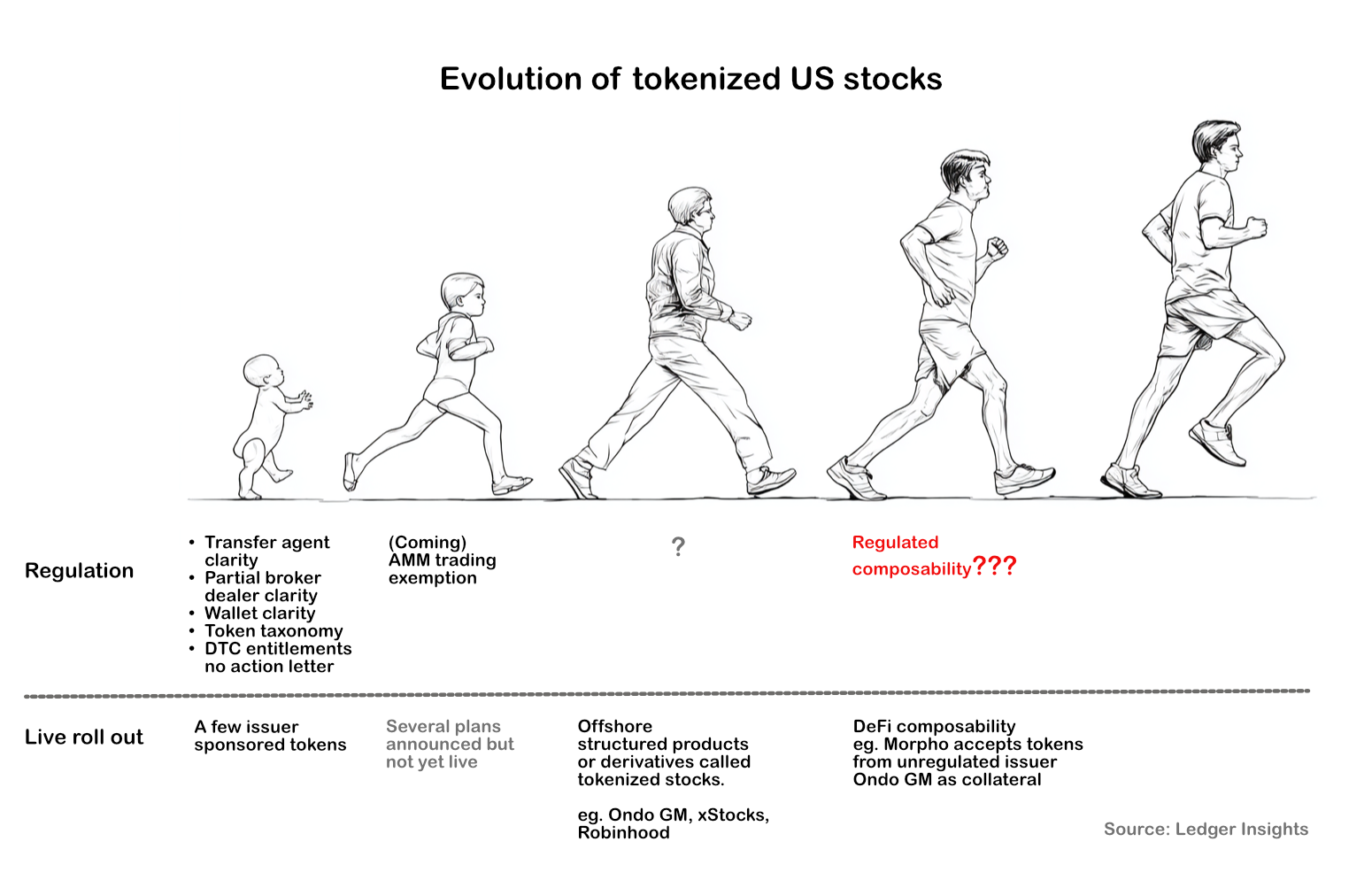

Take Ondo Finance. They’ve got an offshore entity slinging “tokenized stocks” to folks outside the U.S., with actual U.S. stocks held as collateral by some regulated middlemen. Now, their onshore affiliate wants to tokenize the entitlements to those collateral stocks on Ethereum. Ondo’s calling it a ‘recordkeeping innovation.’ Sure. But structurally? It’s pure composability. The solidity of one token rests on another token, which in turn depends on the entire custodial chain. It’s a house of cards, built with very expensive, very digital cards.

The power and the risk lie in the combination.

That quote from the original piece? It’s spot on. The ‘power’ is the potential for massive returns and new market efficiencies. The ‘risk’ is that when one of those components fails – a custodial error, a smart contract bug, a regulatory crackdown – the whole edifice can come crashing down. And who picks up the tab? Usually, it’s not the guys who designed the shiny new toy.

We’re talking about a system where the integrity of one digital representation is tethered to the integrity of another, and so on, all the way down to the physical asset or the legal claim it represents. It’s a chain. And in finance, chains are only as strong as their weakest link. With so many new links being forged at breakneck speed, how many are really up to snuff?

Who’s Actually Cashing In on This Tokenized Frenzy?

This is the evergreen question, isn’t it? Beyond the lofty pronouncements of financial democratization and innovation, who is actually making bank? Right now, it looks like the usual suspects: the asset managers looking for new ways to package and sell risk, the custodians who will hold the underlying assets, the technology providers building the tokenization platforms, and, of course, the lawyers drafting the complex disclosures that attempt to shield everyone from liability. The retail investor, the small business owner, the everyday person who might actually benefit from more accessible markets – they’re usually at the back of the line, holding the bag when things go sideways.

This isn’t to say there’s zero value here. Tokenization could democratize access to certain assets, reduce settlement times, and streamline back-office operations. But let’s not get swept away by the utopian visions peddled by VCs and crypto bros. The fundamental economics of risk and reward haven’t changed. Someone’s taking on risk, and someone’s getting paid handsomely for it. The trick is figuring out if you’re one of the payers or one of the collectors. And with composability, the layers of intermediation can obscure that simple equation until it’s far too late.

Think about the complexity. If you buy a tokenized composite product, and there’s a problem, where do you even start? Do you sue the token issuer? The underlying asset custodian? The platform that facilitated the trade? The smart contract auditor? It’s a regulatory and legal minefield. And in those minefields, the people who profit are the ones who can navigate them best – usually the established financial institutions and their legal teams, not the innovative startups or the individual investors.

We need to see strong regulatory frameworks and standardized practices before we start building entire financial ecosystems on these complex, interconnected tokenized structures. Otherwise, we’re just setting ourselves up for another spectacular, and expensive, implosion. The foundations absolutely must be solid. And right now, they look suspiciously like sand.