Buy Now Pay Later Explained: How BNPL Works and Its Impact on Lending

Buy now pay later has reshaped consumer credit by offering interest-free installment plans at checkout. Understanding how BNPL works reveals both its appeal and its risks.

⚡ Key Takeaways

- {'point': 'Merchant fees drive the BNPL model', 'detail': 'BNPL providers primarily generate revenue by charging merchants 2-8% per transaction, significantly higher than standard credit card interchange fees.'} 𝕏

- {'point': 'Debt invisibility is a key risk', 'detail': 'Consumers can accumulate obligations across multiple BNPL providers that have historically been invisible to credit bureaus, though this is changing as reporting frameworks evolve.'} 𝕏

- {'point': 'Regulation is catching up globally', 'detail': 'Major jurisdictions including the US, UK, EU, and Australia have moved to regulate BNPL providers, requiring affordability checks and consumer protections similar to traditional credit products.'} 𝕏

Worth sharing?

Get the best Finance stories of the week in your inbox — no noise, no spam.

Related Stories

Lending & Credit

Gen Z's BNPL Power Play: No Loyalty, Just Smart Hacks

Digital Banking

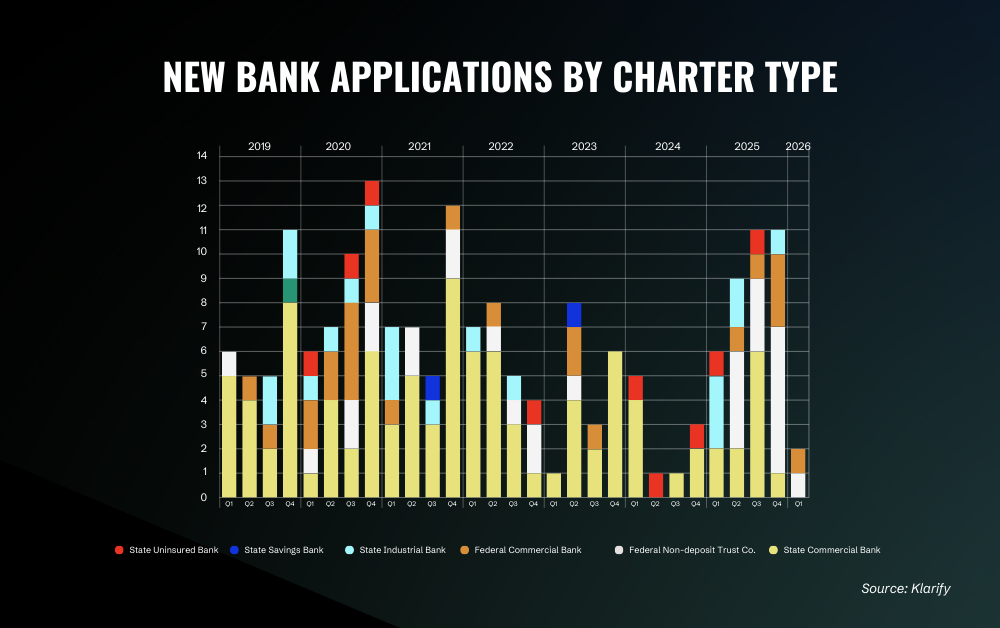

Fintech's Bank Charter Gold Rush: Permits Issued, Picks Raised

RegTech & Compliance

EBA Harmonizes SEPA Reporting: 27 NCAs Unified

Digital Banking